Imagine sitting at your kitchen table in Mesquite, staring at a stack of medical bills that arrived exactly 14 days after your accident. You want to focus on your physical recovery, but the pressure of unpaid expenses and confusing calls from insurance adjusters makes it impossible to rest. You aren’t just looking for a random number; you’re looking for a way to protect your family’s financial stability. It’s completely natural to feel overwhelmed by the legal jargon and the fear that you might be pressured into a settlement that doesn’t cover your true costs.

You deserve a clear, honest look at how the average personal injury settlement amount is actually determined in 2026. This guide will walk you through the specific factors that influence case values, from lost wages to ongoing medical care, so you can set realistic expectations for your claim. You’ll discover the practical steps to maximize your payout and learn how a dedicated local advocate can stand up to big insurance companies on your behalf. Let’s move from a state of uncertainty to a feeling of empowerment together.

Key Takeaways

- Learn why a generic average personal injury settlement amount can be misleading and how to identify the true value of your unique situation.

- Discover the three-part framework used to balance your “hard” medical costs with the “soft” human losses that insurance companies often try to overlook.

- Understand the critical role of insurance policy limits and why finding every available source of coverage is essential to securing the justice you deserve.

- Identify the dangers of settling too early and why reaching Maximum Medical Improvement is the key to protecting your long-term health and finances.

- See how a dedicated legal partner can maximize your actual recovery by negotiating medical liens and standing firm against aggressive insurance tactics.

Understanding the Average Personal Injury Settlement Amount

You are likely facing a mountain of medical bills and the stress of missed paychecks after an accident. A settlement is a voluntary agreement where you agree to resolve your legal dispute in exchange for a specific amount of compensation. It’s a way to find closure without the long, unpredictable path of a full court trial. In the broad field of Personal injury law, these agreements provide the financial lifeline families need to move forward. At the Oberg Law Office, we treat your recovery as our priority, ensuring you don’t feel like just another case number during this difficult time.

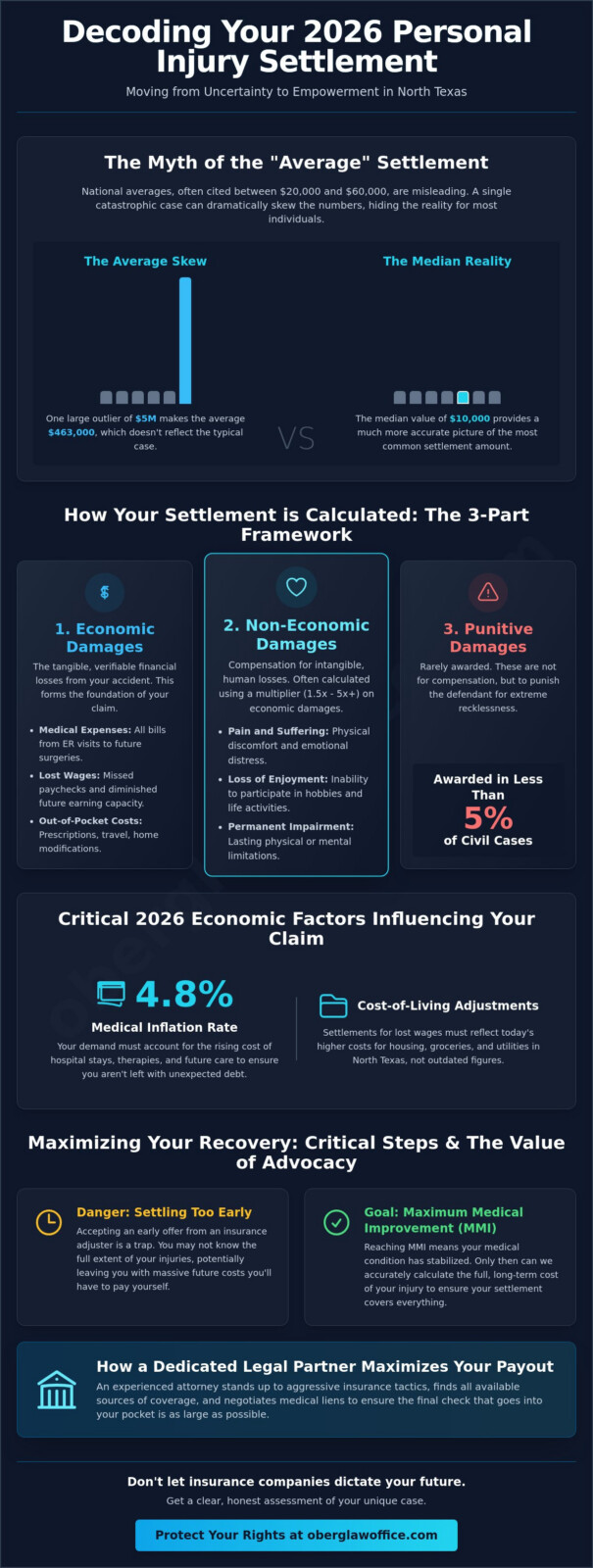

General reports often suggest the average personal injury settlement amount sits between $20,000 and $60,000. These figures can be misleading for individual victims in Mesquite and across Texas. Your specific injuries, the clarity of the other driver’s fault, and the available insurance coverage dictate your case’s true value. While a trial verdict has the potential to reach much higher amounts, it also carries the risk of walking away with nothing. Settlements offer a guaranteed recovery, but national statistics are often skewed by catastrophic cases. When one victim receives a $5 million payout for a permanent disability, it raises the mathematical average for everyone else, even if most payouts are significantly lower.

Average vs. Median: Why the Middle Matters

The “average” is often a poor tool for predicting your results. If ten people receive $10,000 and one person receives $5 million, the average payout looks like $463,000. This doesn’t reflect the reality for the majority of claimants. We prefer to look at the median payout and specific injury tiers. A soft tissue injury or a minor fracture typically falls into a different tier than a surgical requirement or a permanent impairment. Understanding where your injury fits within these tiers provides a much more accurate starting point for our negotiations with insurance adjusters.

The Role of 2026 Economic Trends in Settlements

Economic shifts in 2026 have directly impacted how we calculate your claim’s value. Medical inflation rose by 4.8% this year, which means the “special damages” we demand for your hospital stays and physical therapy must be higher to cover actual costs. We also factor in the 2026 cost-of-living adjustments when we calculate your future lost earning capacity. If you can’t return to work for six months, your settlement must reflect today’s higher grocery, housing, and utility costs in North Texas. We refuse to let insurance companies use outdated 2020 math to settle your 2026 claim.

How Settlement Values are Calculated: The Three-Part Framework

Understanding how your recovery is valued starts with looking at a specific formula. Most insurance adjusters and legal teams use a calculation that combines your tangible receipts with your intangible experiences. While you might be searching for the average personal injury settlement amount, it’s vital to recognize that your case is unique. The “floor” of your claim is always your medical debt, while the “ceiling” is often dictated by insurance policy limits or the severity of the negligence involved.

In rare instances, a third component called punitive damages enters the picture. These aren’t meant to compensate you for a loss; instead, they punish the defendant for especially reckless behavior. While these can exponentially increase a settlement, they are awarded in less than 5% of civil cases nationally. Most of your journey toward justice will focus on the two primary categories below.

Economic Damages: The Foundation of Your Claim

Your economic damages are the “hard costs” that we can verify with a paper trail. As of 2026, medical inflation has shifted how we project your future care needs. We look at every bill from the moment of the accident through your final physical therapy session. If your injuries require home modifications or long-term caregiving, those costs are added to the total. We also document your lost wages and any decrease in your future earning capacity. If you can’t return to your previous career in Mesquite, that financial gap must be bridged. These numbers form the bedrock of your demand letter. You deserve a steadfast protector who ensures not a single receipt is overlooked during this process.

- Medical Expenses: Current bills and projected costs for surgeries or medications.

- Employment Impact: Lost paychecks and the loss of career advancement opportunities.

- Out-of-Pocket Costs: Transportation to specialists and specialized medical equipment for your home.

Non-Economic Damages: Quantifying Pain and Suffering

This is where the calculation becomes more personal. Non-economic damages cover your “soft losses” like emotional trauma, physical pain, and the loss of life’s simple pleasures. Insurance companies often use the Multiplier Method to find a number. They take your total medical bills and multiply them by a factor between 1.5 and 5. A higher multiplier is used when there is permanent scarring or a loss of consortium. According to data regarding Personal Injury Settlement Amounts, the severity of the injury is the primary driver of this multiplier.

Another approach is the Per Diem method. This assigns a specific dollar value to every day you lived in pain during your recovery. If your recovery lasts 250 days and the rate is $200 per day, that adds $50,000 to your claim. Factors like chronic anxiety or the inability to participate in family traditions can significantly push these numbers higher. Every average personal injury settlement amount you see online is influenced by these deeply human factors that a computer program simply cannot feel.

Critical Factors That Swing Your Settlement Value

You might feel frustrated seeing two people with the same injury walk away with vastly different checks. It happens often. The average personal injury settlement amount isn’t just a reflection of your medical bills; it’s a result of several specific variables surrounding your accident. Location plays a massive role in this process. Jurors in different parts of Texas bring different life experiences and expectations to the courtroom. According to Bureau of Justice Statistics trial data, median awards vary significantly by case type and venue, proving that where you file your claim can be just as important as the injury itself.

Insurance Policy Limits and Available Assets

Think of an insurance policy as a bucket. Once it’s empty, there’s nothing left to pour out. This is known as the “policy limit” problem. In Texas, many drivers carry only the state minimum of $30,000 for bodily injury. If your surgery and lost wages total $70,000, that $30,000 policy creates a hard ceiling that often stops your recovery short. We don’t just stop at the first policy we find. Our team digs deeper to identify other “pockets” of recovery, such as umbrella policies or corporate coverage. If a delivery driver or a commercial trucker hits you, there’s often a much larger policy involved. Finding these extra layers of protection is how we make sure your family isn’t left paying for someone else’s mistake.

Liability and the Strength of Evidence

Your payout can be slashed if the insurance company can pin part of the blame on you. Texas follows a “modified comparative negligence” rule. If a jury decides you’re 10% at fault because you were slightly over the speed limit, your settlement is automatically reduced by 10%. If you’re found to be more than 50% responsible, you can’t collect anything at all. This is why we prioritize evidence from the very first day. A mesquite personal injury lawyer moves quickly to preserve dashcam footage, witness statements, and electronic data from the vehicles. When the evidence of the other driver’s fault is undeniable, the insurance company loses its ability to “chip away” at your compensation. Clear liability doesn’t just speed up the process; it forces the insurer to offer a value that truly reflects your losses.

Beyond these factors, the simple credibility of your story matters. When you have a dedicated advocate who treats you like a neighbor rather than a case number, it shows. Insurance adjusters know which firms are prepared to go to trial and which ones just want a quick payout. We stand by you to ensure the final average personal injury settlement amount you receive is fair, just, and enough to actually fund your recovery.

The Settlement Negotiation Timeline: What to Expect

You’re likely feeling the pressure of mounting medical bills and lost wages. It’s natural to want this process to end quickly. However, rushing your claim is exactly what insurance adjusters hope you’ll do. The timeline of your case is a strategic tool. Understanding how it unfolds helps ensure the average personal injury settlement amount you receive actually covers your long-term needs.

Reaching Maximum Medical Improvement (MMI)

Maximum Medical Improvement, or MMI, is the most critical milestone in your recovery. It’s the point where your doctor determines your condition has stabilized as much as it’s going to. You might not feel 100% like your old self, but additional treatment won’t significantly change your outcome. You should never sign a release form until you reach this stage.

If you settle while you’re still healing, you’re essentially guessing at your future costs. Data from the Insurance Research Council suggests that claimants who settle before their medical prognosis is clear often receive significantly less than those who wait. Settling too soon leaves you personally responsible for any “surprise” surgeries or chronic pain management that surfaces six months down the road. MMI provides the final tally for your future medical needs, protecting you from an undervalued claim.

The Anatomy of a Settlement Negotiation

Once your medical team clears you, we assemble a “Demand Package.” This isn’t just a bill; it’s a comprehensive narrative of how the accident changed your life. It includes medical records, expert testimonies, and proof of lost income. In Texas, insurance companies typically have a 30-day window to respond to this demand.

- The Lowball Offer: Expect the first offer to be lower than what you deserve. It’s a test of your patience and your lawyer’s resolve.

- Counter-Offers: We engage in a back-and-forth process, using evidence to push the adjuster toward a fair “bottom line.”

- Complex Timelines: Cases involving a catastrophic injury lawyer often take longer because the evidence required to prove life-altering damages is more extensive.

If the insurance company refuses to meet our demands, we move to mediation or litigation. Mediation involves a neutral third party who helps both sides reach a middle ground. If they still won’t be reasonable, we’re prepared to take your case to a jury. While litigation adds time, it’s often the only way to ensure the average personal injury settlement amount reflects the true level of negligence involved. Our Mesquite team stands with you through every delay and every tactic the insurer uses.

Don’t let an insurance company rush you into a settlement that fails your family. Contact the Oberg Law Office today for a clear-eyed assessment of your case timeline and value.

Maximizing Your Recovery: The Value of Legal Advocacy

Working with a dedicated legal team isn’t just a convenience. It’s a financial necessity for most victims. Data from the Insurance Research Council indicates that settlements for represented claimants are 40% higher than those for people who go it alone. While you’re searching for the average personal injury settlement amount to understand your case’s worth, remember that a lawyer often helps you exceed those baseline numbers by identifying damages you might overlook. We look at the total impact on your life, from future medical needs to the emotional toll on your family.

Our work doesn’t stop at securing a settlement check. We focus on the “net” recovery, which is the actual amount you take home. After an accident, hospitals and health insurance companies often place liens on your settlement to recoup their costs. We negotiate directly with these providers to reduce those liens. By lowering what you owe to third parties, we put more money back into your pocket. It’s about protecting your financial future, not just closing a file.

The “No Fee Unless We Win” promise is our commitment to your recovery. You’ve already been through enough stress. You shouldn’t have to worry about how to afford legal representation. We take on all the financial risk. If we don’t recover money for you, you don’t owe us a dime for our services. This model ensures that everyone has access to high-quality legal help, regardless of their current bank balance. It turns the legal process into a true partnership where our goals are perfectly aligned with yours.

Fighting the Insurance Company’s Tactics

Insurance adjusters are trained to protect their company’s profits. They often use friendly, high-pressure tactics to devalue your claim. A common trick is the “exploding offer,” where they provide a lowball settlement that expires in 24 hours. They want you to sign before you realize the true extent of your injuries. We level the playing field by standing between you and these corporate legal teams. We prepare every case as if it’s heading to a courtroom. When insurers see we’re trial-ready, they’re far more likely to offer a settlement that reflects the true average personal injury settlement amount for your specific injuries.

Your Next Steps Toward Justice

Taking the first step toward recovery is often the hardest part. We make it simple with a free strategy session where we listen to your story and explain your rights. To prepare, try to gather your police reports, medical bills, and any photos from the accident scene. These pieces of evidence are the building blocks of a strong case. Choosing a personal injury lawyer who treats you like a neighbor makes a significant difference in your experience. In our Mesquite office, you’ll speak directly with your attorney. You won’t be passed off to a paralegal. We’re here to provide the personal touch and professional results you deserve. Reach out today to start your journey toward justice.

Protect Your Rights and Your Future

Understanding the factors that influence your compensation is the first step toward reclaiming your life. You’ve seen how medical documentation and liability evidence serve as the foundation for any successful claim. While industry data can provide a broad average personal injury settlement amount, your specific recovery depends on the unique details of your accident and the strength of your legal representation. Every case involves distinct variables that require a tailored approach to ensure you aren’t left paying for someone else’s mistake.

The Oberg Law Office has spent over 25 years fighting for the rights of injury victims in our community. We understand the stress you’re facing; that’s why we offer a clear path forward with zero upfront costs. Our contingency fee model means you pay nothing unless we win your case. When you work with us, you’ll speak directly with your attorney instead of being passed to a staff member. This ensures you receive the personalized attention and seasoned expertise your case deserves. We’re ready to stand as your protector against insurance companies that prioritize profits over people.

Get Your Free Case Strategy Session Today

You’ve been through enough already. Let’s work together to secure the justice and peace of mind you and your family need to move forward.

Frequently Asked Questions

What is the average settlement for a car accident with back pain?

Settlements for back pain typically range from $15,000 for soft tissue strains to over $100,000 for herniated discs that require surgical intervention. Your specific recovery depends on the 2026 medical costs in Mesquite and the documented severity of your injury. We analyze your MRI results and physical therapy records to ensure the insurance company pays for the full impact on your daily life.

How much of my settlement will go to my lawyer?

Most personal injury attorneys in Texas work on a contingency fee basis, which is usually 33.3 percent of the final recovery if the case settles before a lawsuit. This fee may increase to 40 percent if your case requires formal litigation in court. Our office operates on a no fee unless we win model. This means you don’t pay any legal costs unless we successfully recover money for you.

Can I still get a settlement if I was partially at fault?

You can still recover a settlement in Texas as long as your responsibility for the accident is 50 percent or less. Under Texas Civil Practice and Remedies Code Section 33.001, your total compensation is reduced by your specific percentage of fault. If a jury determines you were 20 percent responsible for a $100,000 claim, you’ll receive a check for $80,000. We fight to minimize your fault percentage.

How long does it typically take to receive a settlement check?

You’ll typically receive your settlement check within 30 to 45 days after you sign the final release documents. This period allows the insurance carrier to process the payment and your legal team to resolve any outstanding medical liens with your healthcare providers. We handle the paperwork efficiently so your family can access the funds needed for your recovery without unnecessary waiting periods.

Is a settlement offer from an insurance company final?

A signed settlement release is a legally binding contract that permanently ends your claim against the negligent party and their insurer. Once you accept the funds, you can’t ask for more money later, even if your doctor discovers a new injury related to the crash. It’s vital to have an attorney review any offer to ensure it covers your long term needs before you sign away your rights.

What happens if the settlement offer is lower than my medical bills?

If an offer doesn’t cover your bills, we negotiate with your medical providers to reduce their liens or we prepare to take your case to trial. The average personal injury settlement amount should always account for your total economic losses, including future medical expenses. We don’t let insurance companies push you into a deal that leaves your family with debt after an accident that wasn’t your fault.

Do I have to pay taxes on my personal injury settlement?

Most personal injury settlements are non-taxable under IRS Publication 525 because the money is considered compensation for physical sickness or injury. You won’t owe federal income taxes on the portions of your settlement meant for medical bills, emotional distress, or pain and suffering. However, if your settlement includes punitive damages or specific interest payments, those portions might be subject to taxation by the federal government.

What is the “multiplier method” in personal injury cases?

The multiplier method calculates non-economic damages by multiplying your total medical bills and lost wages by a factor between 1.5 and 5. This calculation helps determine a fair average personal injury settlement amount based on the intensity of your physical pain. A higher multiplier is used for permanent disabilities or life altering injuries that affect your ability to care for your family or enjoy your community.